#SKHynix

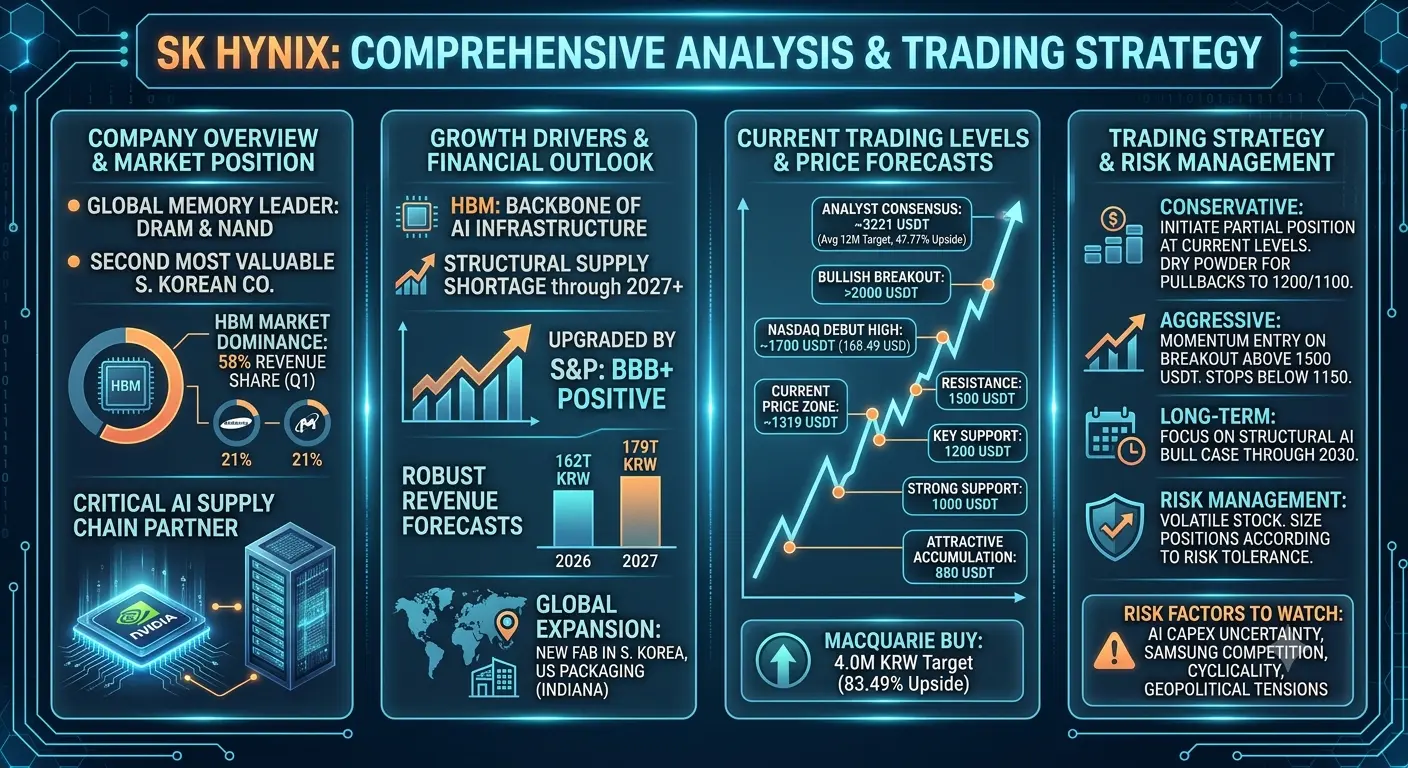

SK Hynix stands as South Korea's second most valuable company, trailing only Samsung Electronics, and ranks among the world's top three memory chip manufacturers alongside Samsung and Micron Technology. The company commands a market capitalization exceeding one trillion dollars, cementing its position as a semiconductor industry powerhouse. SK Hynix specializes in manufacturing DRAM and NAND flash memory chips that power laptops, smartphones, and data centers globally, serving major technology giants including Apple, Dell, HP, Microsoft, and Nvidia.

The crown jewel of SK Hynix's business portfolio is its High Bandwidth Memory segment, commonly known as HBM. This specialized memory technology has become the backbone of artificial intelligence computing infrastructure. SK Hynix currently dominates the HBM market with an impressive 58 percent revenue share in the first quarter, while competitors Samsung and Micron each hold approximately 21 percent market share according to Counterpoint Research data. The company's HBM chips serve as critical components in Nvidia's AI accelerators, positioning SK Hynix at the epicenter of the global AI revolution.

Current Market Position and Recent Developments

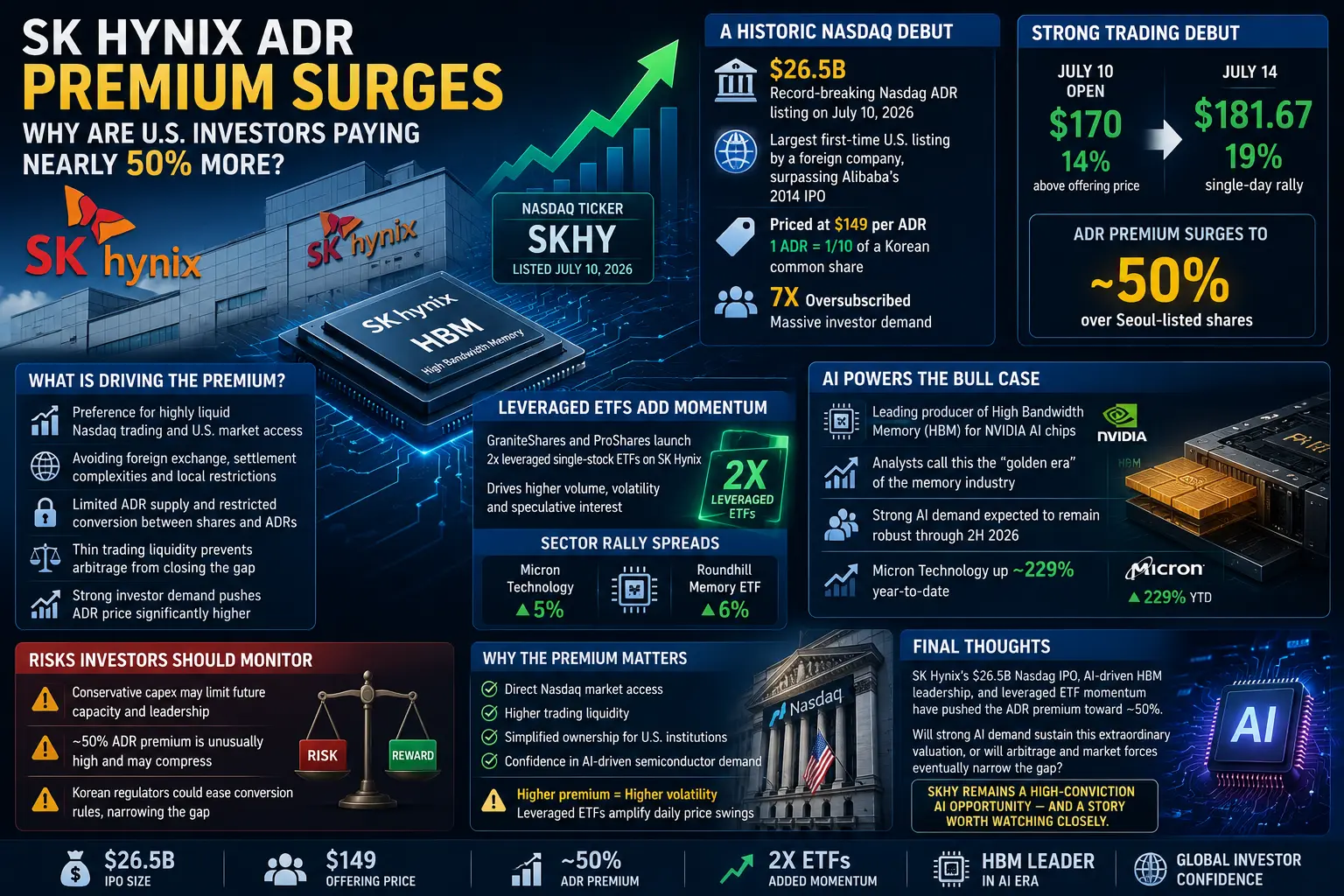

SK Hynix recently completed a landmark initial public offering on the Nasdaq stock exchange, marking the largest-ever US IPO by a foreign company. The company successfully raised 26.5 billion dollars through American Depositary Receipts priced at 149 dollars per share. The Nasdaq debut witnessed remarkable investor enthusiasm, with shares surging 13 percent to 168.49 dollars on the first trading day. However, subsequent sessions have seen profit-taking pressure, with the stock experiencing volatility as investors reassess AI spending sustainability.

The company has outlined ambitious expansion plans utilizing the IPO proceeds. SK Hynix intends to allocate capital toward constructing a new fabrication facility in South Korea, establishing an advanced packaging facility, and procuring EUV scanners to address surging HBM demand. Additionally, the company announced a 4 billion dollar HBM facility investment in Indiana, United States, demonstrating its commitment to geographic diversification and proximity to key customers.

Supply and Demand Dynamics

The memory semiconductor market faces unprecedented supply constraints that favor established manufacturers. CEO Kwak Noh-jung delivered a stark warning that 2027 will represent the worst supply shortage in industry history. Demand for memory chips continues to outstrip production capacity, with this imbalance projected to persist beyond 2030 despite aggressive capacity expansion initiatives. This structural supply deficit creates a favorable pricing environment for SK Hynix and its competitors.

Samsung and SK Hynix have jointly committed 518 billion dollars toward building four new memory manufacturing facilities and an HBM packaging hub in South Korea's Southwest Region over the coming decade. This massive capital expenditure underscores the industry's confidence in sustained demand growth driven by AI infrastructure buildout.

Financial Performance and Analyst Sentiment

S&P Global Ratings recently upgraded SK Hynix to BBB plus with a positive outlook, citing expectations of robust operating performance over the next one to two years. The rating agency anticipates significant growth in sales of highly profitable HBM chips while supply shortages push conventional memory prices higher. S&P forecasts SK Hynix revenue reaching 162 trillion Korean Won in 2026 and 179 trillion Korean Won in 2027. EBITDA projections stand at 112 trillion Korean Won and 116 trillion Korean Won respectively.

Analyst consensus remains overwhelmingly bullish on SK Hynix prospects. Thirty-seven analysts covering the stock have established an average twelve-month price target of 3,221,475 Korean Won, representing approximately 47.77 percent upside potential from current levels. The high analyst estimate reaches 4,700,000 Korean Won while the low estimate sits at 1,030,000 Korean Won. Macquarie maintains a Buy rating with a 4,000,000 Korean Won price target, suggesting 83.49 percent upside potential.

Current Price Analysis and Technical Levels

The stock currently trades at approximately 1319 USDT equivalent, experiencing recent volatility following the Nasdaq listing euphoria. Technical analysis reveals several critical support and resistance levels that traders should monitor closely.

Key support levels include 1200 USDT, representing a psychological round number and recent consolidation area. Below this, 1100 USDT provides secondary support, while 1000 USDT marks a major technical floor where substantial buying interest should emerge. The 880 USDT level coincides with accumulated volume support and would represent an attractive accumulation zone for long-term investors.

Resistance levels begin at 1500 USDT, where recent selling pressure has capped advances. Above this, 1700 USDT aligns with the Nasdaq debut high of 168.49 dollars and represents significant psychological resistance. The 2000 USDT level marks a major technical barrier that would confirm a renewed uptrend if breached. A decisive breakout above 2200 USDT would target the analyst consensus price target zone near 3221 USDT equivalent.

Trading Strategy and Recommendations

For conservative investors seeking exposure to the AI memory theme, current levels near 1319 USDT present a reasonable entry point. The strategy involves initiating a partial position immediately while maintaining dry powder for potential pullbacks toward 1200 USDT or 1100 USDT support zones. Dollar-cost averaging over multiple entry points reduces timing risk in this volatile semiconductor stock.

Aggressive traders might employ a momentum-based approach, waiting for a decisive breakout above 1500 USDT resistance before initiating long positions. This strategy sacrifices some upside potential in exchange for confirmation of trend resumption. Stop-loss orders should be placed below 1150 USDT to limit downside risk.

Long-term investors should focus on the structural bull case rather than short-term price fluctuations. The HBM supply shortage extending through 2030 provides a multi-year tailwind for SK Hynix earnings growth. Accumulating shares during market weakness and holding through volatility aligns with the fundamental investment thesis.

Risk management remains paramount given the stock's inherent volatility. Position sizing should reflect individual risk tolerance, with semiconductor stocks typically warranting smaller allocations than defensive sectors. Portfolio diversification across multiple AI beneficiaries reduces company-specific risk while maintaining thematic exposure.

Risk Factors and Considerations

Several risks warrant careful monitoring. Cloud service providers might reduce capital expenditure on AI infrastructure if return on investment fails to meet expectations, directly impacting HBM demand. Samsung Electronics continues investing heavily to catch up in HBM technology, potentially eroding SK Hynix's market leadership over time. Memory chip prices exhibit cyclical patterns, and the current upcycle will eventually normalize, compressing margins across the industry.

Geopolitical tensions involving South Korea, China, or the United States could disrupt supply chains or limit market access. Trade policy changes affecting semiconductor equipment or raw materials would impact production costs and competitiveness. Currency fluctuations between the Korean Won and US Dollar create translation effects for international investors.

Market Outlook and Price Forecasts

The near-term outlook remains constructive despite recent volatility. The AI infrastructure buildout shows no signs of slowing, with hyperscalers continuing massive investments in data center capacity. SK Hynix's dominant HBM position and Nvidia partnership provide competitive moats that should sustain premium valuations.

Medium-term price targets suggest significant upside potential. Conservative scenarios project 1800 USDT by year-end 2026, representing approximately 36 percent appreciation from current levels. Bull case scenarios targeting 2200 USDT or higher depend on continued AI spending momentum and successful execution of capacity expansion plans.

Long-term investors should focus on the 2027-2030 horizon when supply shortages peak and SK Hynix's expanded capacity comes online. The company expects to double memory wafer production over five years, positioning it to capture substantial revenue growth as demand continues expanding.

Conclusion

SK Hynix represents a compelling investment opportunity at the intersection of artificial intelligence infrastructure and semiconductor memory technology. The company's dominant HBM market position, strong Nvidia partnership, and massive capacity expansion plans align with multi-year demand tailwinds. Current price levels near 1319 USDT offer attractive entry points for investors willing to navigate near-term volatility.

The structural supply shortage extending through 2030 provides pricing power and earnings visibility rarely seen in the cyclical semiconductor industry. While risks exist regarding competition and demand sustainability, the risk-reward profile favors long-term accumulation at current levels. Traders should employ disciplined risk management while maintaining exposure to this critical AI supply chain beneficiary.

The memory semiconductor sector stands at the beginning of what industry executives describe as a golden era. SK Hynix, with its technological leadership and strategic positioning, appears well-equipped to capture substantial value creation throughout this transformational period in computing history.

SK Hynix stands as South Korea's second most valuable company, trailing only Samsung Electronics, and ranks among the world's top three memory chip manufacturers alongside Samsung and Micron Technology. The company commands a market capitalization exceeding one trillion dollars, cementing its position as a semiconductor industry powerhouse. SK Hynix specializes in manufacturing DRAM and NAND flash memory chips that power laptops, smartphones, and data centers globally, serving major technology giants including Apple, Dell, HP, Microsoft, and Nvidia.

The crown jewel of SK Hynix's business portfolio is its High Bandwidth Memory segment, commonly known as HBM. This specialized memory technology has become the backbone of artificial intelligence computing infrastructure. SK Hynix currently dominates the HBM market with an impressive 58 percent revenue share in the first quarter, while competitors Samsung and Micron each hold approximately 21 percent market share according to Counterpoint Research data. The company's HBM chips serve as critical components in Nvidia's AI accelerators, positioning SK Hynix at the epicenter of the global AI revolution.

Current Market Position and Recent Developments

SK Hynix recently completed a landmark initial public offering on the Nasdaq stock exchange, marking the largest-ever US IPO by a foreign company. The company successfully raised 26.5 billion dollars through American Depositary Receipts priced at 149 dollars per share. The Nasdaq debut witnessed remarkable investor enthusiasm, with shares surging 13 percent to 168.49 dollars on the first trading day. However, subsequent sessions have seen profit-taking pressure, with the stock experiencing volatility as investors reassess AI spending sustainability.

The company has outlined ambitious expansion plans utilizing the IPO proceeds. SK Hynix intends to allocate capital toward constructing a new fabrication facility in South Korea, establishing an advanced packaging facility, and procuring EUV scanners to address surging HBM demand. Additionally, the company announced a 4 billion dollar HBM facility investment in Indiana, United States, demonstrating its commitment to geographic diversification and proximity to key customers.

Supply and Demand Dynamics

The memory semiconductor market faces unprecedented supply constraints that favor established manufacturers. CEO Kwak Noh-jung delivered a stark warning that 2027 will represent the worst supply shortage in industry history. Demand for memory chips continues to outstrip production capacity, with this imbalance projected to persist beyond 2030 despite aggressive capacity expansion initiatives. This structural supply deficit creates a favorable pricing environment for SK Hynix and its competitors.

Samsung and SK Hynix have jointly committed 518 billion dollars toward building four new memory manufacturing facilities and an HBM packaging hub in South Korea's Southwest Region over the coming decade. This massive capital expenditure underscores the industry's confidence in sustained demand growth driven by AI infrastructure buildout.

Financial Performance and Analyst Sentiment

S&P Global Ratings recently upgraded SK Hynix to BBB plus with a positive outlook, citing expectations of robust operating performance over the next one to two years. The rating agency anticipates significant growth in sales of highly profitable HBM chips while supply shortages push conventional memory prices higher. S&P forecasts SK Hynix revenue reaching 162 trillion Korean Won in 2026 and 179 trillion Korean Won in 2027. EBITDA projections stand at 112 trillion Korean Won and 116 trillion Korean Won respectively.

Analyst consensus remains overwhelmingly bullish on SK Hynix prospects. Thirty-seven analysts covering the stock have established an average twelve-month price target of 3,221,475 Korean Won, representing approximately 47.77 percent upside potential from current levels. The high analyst estimate reaches 4,700,000 Korean Won while the low estimate sits at 1,030,000 Korean Won. Macquarie maintains a Buy rating with a 4,000,000 Korean Won price target, suggesting 83.49 percent upside potential.

Current Price Analysis and Technical Levels

The stock currently trades at approximately 1319 USDT equivalent, experiencing recent volatility following the Nasdaq listing euphoria. Technical analysis reveals several critical support and resistance levels that traders should monitor closely.

Key support levels include 1200 USDT, representing a psychological round number and recent consolidation area. Below this, 1100 USDT provides secondary support, while 1000 USDT marks a major technical floor where substantial buying interest should emerge. The 880 USDT level coincides with accumulated volume support and would represent an attractive accumulation zone for long-term investors.

Resistance levels begin at 1500 USDT, where recent selling pressure has capped advances. Above this, 1700 USDT aligns with the Nasdaq debut high of 168.49 dollars and represents significant psychological resistance. The 2000 USDT level marks a major technical barrier that would confirm a renewed uptrend if breached. A decisive breakout above 2200 USDT would target the analyst consensus price target zone near 3221 USDT equivalent.

Trading Strategy and Recommendations

For conservative investors seeking exposure to the AI memory theme, current levels near 1319 USDT present a reasonable entry point. The strategy involves initiating a partial position immediately while maintaining dry powder for potential pullbacks toward 1200 USDT or 1100 USDT support zones. Dollar-cost averaging over multiple entry points reduces timing risk in this volatile semiconductor stock.

Aggressive traders might employ a momentum-based approach, waiting for a decisive breakout above 1500 USDT resistance before initiating long positions. This strategy sacrifices some upside potential in exchange for confirmation of trend resumption. Stop-loss orders should be placed below 1150 USDT to limit downside risk.

Long-term investors should focus on the structural bull case rather than short-term price fluctuations. The HBM supply shortage extending through 2030 provides a multi-year tailwind for SK Hynix earnings growth. Accumulating shares during market weakness and holding through volatility aligns with the fundamental investment thesis.

Risk management remains paramount given the stock's inherent volatility. Position sizing should reflect individual risk tolerance, with semiconductor stocks typically warranting smaller allocations than defensive sectors. Portfolio diversification across multiple AI beneficiaries reduces company-specific risk while maintaining thematic exposure.

Risk Factors and Considerations

Several risks warrant careful monitoring. Cloud service providers might reduce capital expenditure on AI infrastructure if return on investment fails to meet expectations, directly impacting HBM demand. Samsung Electronics continues investing heavily to catch up in HBM technology, potentially eroding SK Hynix's market leadership over time. Memory chip prices exhibit cyclical patterns, and the current upcycle will eventually normalize, compressing margins across the industry.

Geopolitical tensions involving South Korea, China, or the United States could disrupt supply chains or limit market access. Trade policy changes affecting semiconductor equipment or raw materials would impact production costs and competitiveness. Currency fluctuations between the Korean Won and US Dollar create translation effects for international investors.

Market Outlook and Price Forecasts

The near-term outlook remains constructive despite recent volatility. The AI infrastructure buildout shows no signs of slowing, with hyperscalers continuing massive investments in data center capacity. SK Hynix's dominant HBM position and Nvidia partnership provide competitive moats that should sustain premium valuations.

Medium-term price targets suggest significant upside potential. Conservative scenarios project 1800 USDT by year-end 2026, representing approximately 36 percent appreciation from current levels. Bull case scenarios targeting 2200 USDT or higher depend on continued AI spending momentum and successful execution of capacity expansion plans.

Long-term investors should focus on the 2027-2030 horizon when supply shortages peak and SK Hynix's expanded capacity comes online. The company expects to double memory wafer production over five years, positioning it to capture substantial revenue growth as demand continues expanding.

Conclusion

SK Hynix represents a compelling investment opportunity at the intersection of artificial intelligence infrastructure and semiconductor memory technology. The company's dominant HBM market position, strong Nvidia partnership, and massive capacity expansion plans align with multi-year demand tailwinds. Current price levels near 1319 USDT offer attractive entry points for investors willing to navigate near-term volatility.

The structural supply shortage extending through 2030 provides pricing power and earnings visibility rarely seen in the cyclical semiconductor industry. While risks exist regarding competition and demand sustainability, the risk-reward profile favors long-term accumulation at current levels. Traders should employ disciplined risk management while maintaining exposure to this critical AI supply chain beneficiary.

The memory semiconductor sector stands at the beginning of what industry executives describe as a golden era. SK Hynix, with its technological leadership and strategic positioning, appears well-equipped to capture substantial value creation throughout this transformational period in computing history.