The question: Do users need to pay taxes when buying American stocks on Gate matters, because buying American stocks through a crypto platform can involve more than one financial layer. A user may hold USDT, transfer funds into a stock account, buy a supported US stock or ETF, receive dividend-related benefits, and later sell or withdraw funds. Each step may have a different tax meaning depending on the user’s country or region.

The digital asset value of this model is that users can access stock exposure through crypto balances rather than a traditional bank funding route. That can simplify asset movement inside a digital asset account, but it does not remove tax, reporting, or documentation responsibilities.

Do Users Need to Pay Taxes When Buying American Stocks on Gate? Definition and Scope

The safest answer is that users may have tax or reporting obligations, but there is no single global rule for every user. Tax depends on where the user is a tax resident, how the USDT was obtained, whether a stock position is sold, whether dividends are received, and how local law classifies both digital assets and foreign stock exposure.

A stock purchase alone may not always create immediate tax due in some jurisdictions. However, the broader path may still include taxable events. For example, a user who sells BTC or ETH to obtain USDT may need to calculate a gain or loss before the stock purchase even happens. A user who later sells a US stock position may also need to calculate realized gain or loss. If the stock or ETF pays a dividend, that dividend may be treated as income and may also involve U.S.-source withholding rules for some non-U.S. users.

Gate Stocks should therefore be understood as a market access mechanism, not as a tax-free structure. Users can review how Gate Stocks trading works to understand the operational model, while separately checking their own tax position. The platform workflow and the user’s tax outcome are related, but they are not the same thing.

Risk reminder: Tax rules can change and may differ across jurisdictions. This content is for educational purposes only and does not constitute tax, legal, financial, or investment advice.

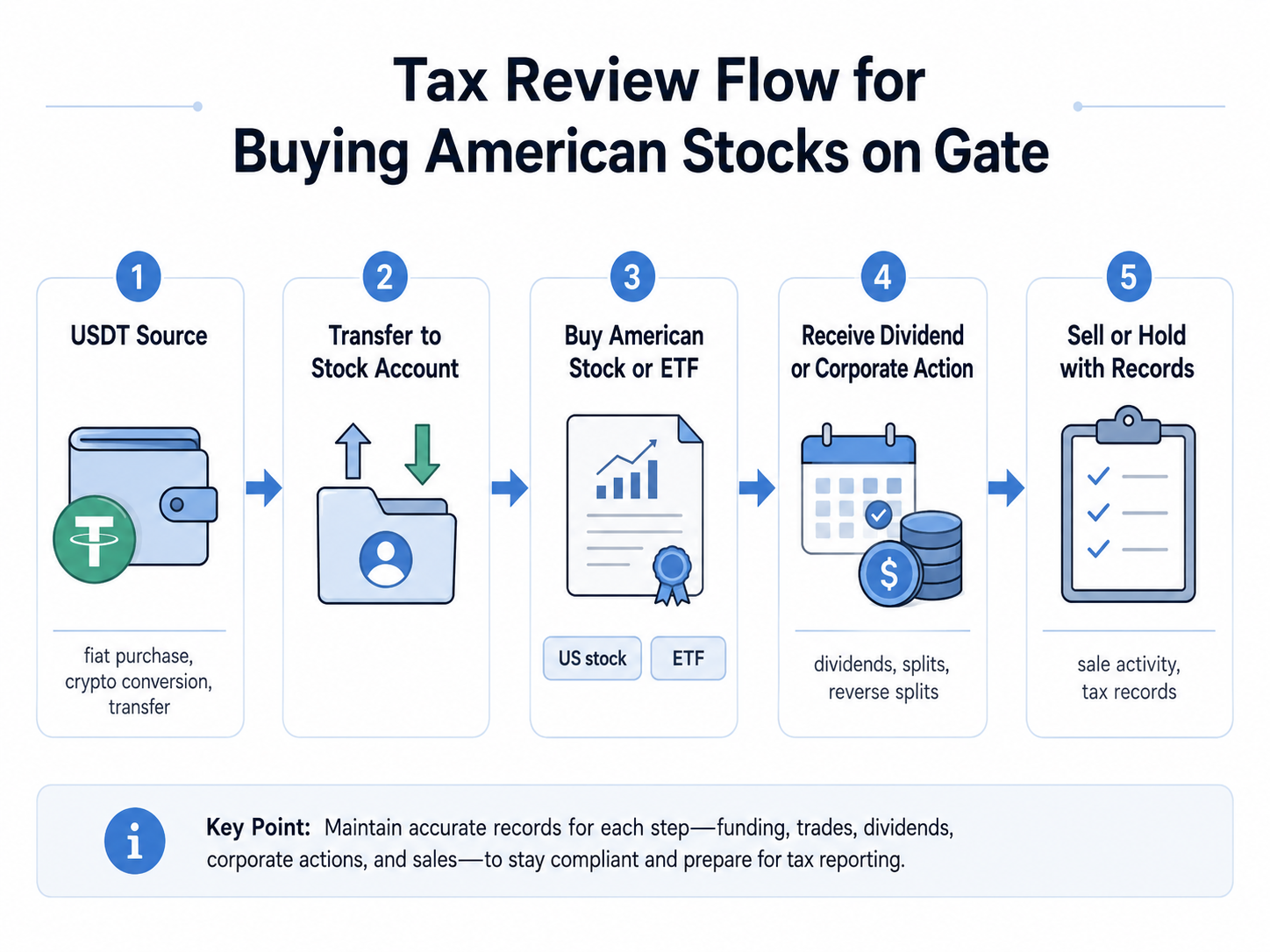

How Tax Review Works When Buying American Stocks on Gate

Tax review works by separating the user journey into events. Instead of asking only whether the buy button creates tax, users should review the full chain: where the USDT came from, how it was transferred, what was purchased, whether income was received, and what happened later.

A typical sequence may look like this:

Step 1: Identify the USDT source.

USDT may come from fiat purchase, crypto conversion, platform balance, transfer from another wallet, rewards, or income. The source affects whether a prior taxable event may already exist.

Step 2: Check whether a crypto disposal occurred.

If another digital asset was sold or swapped into USDT, some tax systems may treat that as a disposal. A gain or loss may need to be calculated using cost basis and fair market value.

Step 3: Confirm the stock or ETF purchase record.

Users should keep order records, date, asset name, quantity, purchase value, and fees. A purchase record becomes important later if the position is sold.

Step 4: Track dividends and corporate actions. Supported cash dividends, stock dividends, splits, and reverse splits may affect income records or cost basis. The distinction between economic benefits and shareholder rights can be understood through Gate Stocks economic rights and shareholder rights.

Step 5: Review sale, withdrawal, or conversion events.

When a stock position is sold, or when proceeds are converted or withdrawn, additional reporting may be required depending on local rules.

| Preparation Area |

What to Check |

Why It Matters |

| Tax residency |

Country or region where the user is tax resident |

Tax residency usually determines the reporting framework |

| USDT source |

Fiat purchase, crypto conversion, income, rewards, or transfer |

The source may affect cost basis and taxable-event review |

| Product type |

Stock, ETF, CFD, tokenized stock, or other exposure |

Different products may receive different tax treatment |

| Purchase record |

Date, asset, quantity, value, and fees |

Needed for future gain or loss calculation |

| Dividend record |

Dividend date, amount, withholding, and credited balance |

Dividends may be taxable income |

| Sale record |

Sale date, proceeds, fees, and realized result |

Selling may create capital gain or loss |

| Local rules |

Crypto, foreign asset, dividend, and capital gains rules |

The same transaction may be treated differently by jurisdiction |

These preparation points matter because a tax answer cannot be based only on the final purchase screen. A complete record trail gives users a clearer basis for reporting and for discussing the transaction with a qualified tax professional. Users who want to understand the USDT-funded access path can compare it with buying US stocks with USDT, where the funding route, account movement, and order process are part of the broader user journey.

Do Users Need to Pay Taxes When Buying American Stocks on Gate? Comparison With Other Access Models

The tax question becomes clearer when Gate Stocks is compared with traditional brokerage accounts, CFDs, and tokenized stock models. The economic exposure may look similar to the user, but the product structure, funding method, record type, and tax review points can differ.

| Comparison Dimension |

Buying American Stocks on Gate |

Traditional Brokerage Account |

Stock CFD |

Tokenized Stock |

| Funding route |

Usually digital asset balance such as USDT |

Fiat bank transfer or broker-supported funding |

Fiat or margin balance |

Crypto or stablecoin balance |

| Main user record |

USDT movement, stock order, income, sale history |

Broker statements and tax forms |

Contract entry, exit, fees, and financing |

Token purchase, sale, redemption, and issuer terms |

| Product structure |

Platform-supported stock or ETF access |

Securities account structure |

Derivative contract based on price difference |

Token or platform representation of stock exposure |

| Dividend handling |

May support dividend-related economic benefits |

Broker dividend records may apply |

Usually no direct shareholder dividend ownership |

Depends on issuer terms |

| Shareholder rights |

Certain registered shareholder rights may not apply |

More direct traditional shareholder framework |

No shareholder rights |

Usually limited or no direct shareholder rights |

| Main tax focus |

USDT source, stock sale, dividend income, local reporting |

Stock gains, dividends, broker tax forms |

Derivative gains, financing, local rules |

Token disposal, income treatment, issuer terms |

| Recordkeeping difficulty |

Requires crypto and stock records together |

Usually centralized broker reporting |

Requires derivative trade tracking |

Requires token and issuer record review |

The comparison shows why users should not assume that every product connected to American stocks is treated the same way. A traditional broker, a CFD platform, a tokenized stock issuer, and a USDT-funded stock access model can produce different documentation and different tax questions. Understanding Gate Stocks compared with brokers and stock CFDs helps users identify which records may matter most.

This comparison is also important for users who already trade digital assets. Crypto-funded market access introduces a funding layer that may not exist in a traditional stock account. A user may need to calculate both digital asset events and stock-related events. That does not mean tax is always due at every step, but it does mean users should avoid treating the process as a single simple stock purchase.

Risks, Limitations, and Misconceptions About Taxes When Buying American Stocks on Gate

The biggest misconception is that using USDT automatically avoids tax. In many jurisdictions, digital assets are reportable or taxable when sold, exchanged, received as income, or otherwise disposed of. Stablecoins may also require recordkeeping even when their market value is designed to track the US dollar.

Another misconception is that tax only matters after a stock is sold. In reality, a prior crypto conversion may have already created a taxable event. Dividend income may also be relevant even if the user has not sold the stock position. If the dividend is connected to a U.S.-source stock or ETF, non-U.S. users may need to consider withholding, tax treaty rules, and local reporting.

Users should also avoid assuming that platform records replace personal tax responsibility. Account history may help, but it may not classify every event under the user’s local tax code. Local rules can differ on digital asset cost basis, foreign asset reporting, dividend income, capital gains, and whether stablecoin use is treated as disposal.

Operational risk also matters. Missing transaction records, incorrect timestamps, incomplete cost basis, and mixed wallet transfers can make tax reporting more difficult. Users who access other traditional asset categories with crypto balances, such as trading gold, silver, and oil with crypto assets, may face similar recordkeeping issues. The asset type changes, but the need to document funding, income, and settlement remains.

Risk reminder: Regulatory, tax, liquidity, product-structure, custody, and reporting risks may apply. Users should verify local rules and consult a qualified tax professional where needed.

Summary

Do users need to pay taxes when buying American stocks on Gate? The answer depends on the user’s jurisdiction and transaction history. A purchase may not always create immediate tax due, but surrounding events can still matter.

The key review areas are USDT acquisition, crypto-to-USDT conversion, stock or ETF purchase records, dividend income, corporate actions, sale of the position, withdrawal or conversion after sale, and local reporting rules. Users should separate the digital asset layer from the stock layer because each may follow different tax logic.

Gate Stocks can provide crypto-funded access to supported American stocks and ETFs, but the platform mechanism does not remove tax obligations. A careful user should keep complete records, understand product structure, avoid assuming that stablecoin use is tax-neutral, and seek professional advice when rules are unclear.

This content is for educational purposes only and does not constitute tax, legal, financial, or investment advice. Digital assets and stock-related products can involve market, liquidity, custody, operational, tax, and regulatory risks.

FAQs

Do users need to pay taxes when buying American stocks on Gate?

Do users need to pay taxes when buying American stocks on Gate depends on tax residency, local rules, and the full transaction path. A user may need to review USDT source, crypto conversions, dividend income, and later sale activity before deciding whether tax is due.

Do users need to pay taxes when buying American stocks on Gate if they only buy and hold?

Do users need to pay taxes when buying American stocks on Gate if they only buy and hold depends on how the USDT was obtained and whether any income was received. If the user converted another crypto asset into USDT before buying, that earlier conversion may still be relevant.

Do users need to pay taxes when buying American stocks on Gate with USDT?

Do users need to pay taxes when buying American stocks on Gate with USDT depends on whether using USDT is treated as a digital asset disposal in the user’s jurisdiction. Even if no immediate stock tax applies, USDT records may still be needed.

Are dividends from American stocks on Gate taxable?

Dividends may be taxable income depending on the user’s local rules. If the dividend is treated as U.S.-source income, withholding rules or treaty rates may also be relevant for some non-U.S. users.

Is buying American stocks on Gate the same as using a traditional broker for tax purposes?

It may not be the same because the funding route, product structure, and record format can differ. A traditional broker may provide different tax forms, while a USDT-funded platform flow may require users to track both digital asset and stock-related records.

What records should users keep for American stock purchases on Gate?

Users should keep USDT source records, crypto conversion history, internal transfer records, stock order confirmations, dividend records, corporate action details, fees, sale records, and withdrawal or conversion history. These records help calculate possible gains, losses, income, and reporting obligations.